Was du über Hypercar-Versicherungen nicht weißt – aber wissen solltest!

Hypercars wie der Bugatti Chiron sind Meisterwerke der Technik – doch ihre Absicherung erfordert mehr als eine Standardversicherung.

Kapitel 1: Warum Hypercar-Versicherungen ein ganz eigenes Thema sind

Wenn du denkst, eine Kfz-Versicherung sei einfach nur ein lästiger Pflichtbeitrag, dann hast du wahrscheinlich noch nie ein Hypercar besessen. Denn sobald ein Fahrzeug jenseits der 1-Million-Euro-Marke rangiert, mit 1.000+ PS über die Straße (oder Rennstrecke) schießt und aus limitierten Serien stammt, beginnt eine völlig andere Welt – auch versicherungstechnisch.

Exotik bringt Extrarisiken mit sich

Hypercars wie der Bugatti Chiron, Koenigsegg Jesko oder Pagani Huayra sind keine gewöhnlichen Fortbewegungsmittel – sie sind rollende Kunstwerke, technologische Meisterleistungen und Prestigeobjekte. Genau das macht ihre Versicherung so speziell. Hier geht es nicht nur um einfache Schäden durch Unfälle oder Diebstahl, sondern auch um Risiken wie:

Transport- und Verschiffungsschäden (z. B. bei Auslieferung, Events, Trackdays)

Motor- oder Getriebeschäden durch extreme Belastung

Schäden bei nicht-öffentlichen Fahrveranstaltungen (z. B. Nürburgring-Nordschleife)

Vandalismus oder gezielter Diebstahl durch organisierte Banden

Standard reicht nicht – und wird oft gar nicht angeboten

Viele herkömmliche Versicherer lehnen Hypercars schlichtweg ab – nicht nur wegen der hohen Summen, sondern weil die Risikobewertung viel komplexer ist. Einige Versicherer verlangen beispielsweise Sicherheitsvorkehrungen wie:

Videoüberwachtes Einzelstellplatz-Garagenkonzept

GPS-gestütztes Ortungssystem mit Notruffunktion

Nutzungseinschränkungen (z. B. keine Nutzung im Winter oder auf öffentlichen Trackdays)

Selbst wenn eine Standardversicherung den Abschluss zulassen würde, wären die Deckungssummen meist völlig unzureichend – und im Ernstfall steht der Halter mit einem Totalschaden ohne adäquaten Ersatz da.

Es geht nicht nur um Geld – sondern um Vertrauen

Eine Hypercar-Versicherung ist nicht einfach ein Produkt, sondern eine persönliche Beziehung zwischen Halter, Versicherungsmakler und Versicherer. Oft arbeiten Sammler und Besitzer mit spezialisierten Anbietern, die auf exklusive Fahrzeuge, Oldtimer und rare Supersportwagen spezialisiert sind. In vielen Fällen werden Policen individuell angepasst – je nach Fahrverhalten, Abstellort, internationaler Nutzung und geplanten Events.

Gerade bei stark limitierten Modellen – etwa einem Ferrari LaFerrari Aperta oder einem McLaren Speedtail – kann der Verlust eines Fahrzeugs nicht nur finanziell, sondern auch emotional und sammlerbezogen ein schwerwiegender Schlag sein. Der Wertverlust durch nicht mehr originalgetreue Ersatzteile oder Reparaturen durch nicht-akkreditierte Werkstätten kann enorm sein.

Wer sich ein Hypercar leisten kann, unterschätzt oft die Bedeutung einer präzise abgestimmten Versicherung. Denn hier geht es nicht nur darum, „abgesichert“ zu sein, sondern um den Erhalt von Wert, Seltenheit und Performance – und damit um weit mehr als nur eine Police auf Papier. Eine maßgeschneiderte Versicherung gehört zum Hypercar genauso wie Carbon, Titan und aktive Aerodynamik – nur eben im Hintergrund.

Kapitel 2: Grundlagen – Was eine Hypercar-Versicherung überhaupt ist

2.1 Definition eines Hypercars

Der Begriff „Hypercar“ wird oft verwendet, aber nur selten klar definiert. Im Kern beschreibt er Fahrzeuge, die in jeder Hinsicht an die Grenzen des technisch Machbaren gehen. Hypercars sind die Speerspitze der Automobiltechnik – und das betrifft Leistung, Design, Materialien und Exklusivität gleichermaßen.

Im Gegensatz zu Supersportwagen wie einem Porsche 911 Turbo S oder einem Audi R8, die noch in größerer Stückzahl produziert werden, sind Hypercars fast immer:

Extrem limitiert (z. B. „1 of 99“ oder weniger)

Mit enormen Leistungsdaten ausgestattet (häufig über 1.000 PS)

Preislich deutlich über der Millionengrenze angesiedelt

Technologisch experimentell oder bahnbrechend (z. B. aktives Fahrwerk, Hybridantriebe, Carbon-Monocoques)

Marken wie Bugatti, Koenigsegg, Pagani, McLaren (z. B. Speedtail), Rimac und Ferrari (z. B. LaFerrari) gelten als typische Hypercar-Hersteller. In jüngerer Zeit stoßen auch Newcomer wie Czinger oder De Tomaso mit extrem limitierten Modellen dazu.

Diese Fahrzeuge sind nicht nur Sammlerobjekte – sie sind Hochleistungsmaschinen mit komplexer Technik und hohem Marktwert. Genau das macht sie auch versicherungstechnisch zu einer völlig eigenen Klasse.

2.2 Abgrenzung zu normalen Kfz-Versicherungen

Eine normale Kfz-Versicherung besteht aus drei Bausteinen: Haftpflichtversicherung, Teilkasko und Vollkasko. Diese decken üblicherweise Schäden an Dritten, Diebstahl, Glasbruch oder Unfälle ab – auf Grundlage von Zeitwerten, Typklassen und Schadenfreiheitsrabatten.

Doch bei einem Hypercar wie einem Pagani Huayra BC oder einem Koenigsegg Jesko ist dieses System nicht mehr ausreichend:

Typklassen greifen nicht: Für ein Fahrzeug, das in Deutschland nur in ein oder zwei Exemplaren zugelassen ist, existiert keine fundierte statistische Risikobasis.

Zeitwertprinzip ist ungeeignet: Viele Hypercars steigen im Wert – insbesondere, wenn sie selten gefahren, gepflegt und gut gelagert werden. Eine „Wertminderung durch Alter“ ist hier schlichtweg unrealistisch.

Werkstattbindung ist problematisch: Normale Versicherer verlangen oft die Nutzung von Partnerwerkstätten – doch für ein Fahrzeug aus einer Kleinserie mit Titan-Schrauben und handgefertigtem Interieur gibt es meist nur eine Handvoll Spezialisten weltweit.

Auch der administrative Ablauf unterscheidet sich: Während normale Policen oft online abschließbar sind, werden Hypercar-Versicherungen meist individuell kalkuliert. Es gibt keine Tarifrechner – stattdessen fließen Faktoren wie Lagerbedingungen, Marktwertgutachten, Trackday-Nutzung oder internationale Transporte in die Bewertung ein.

Ein weiterer Punkt: Viele Versicherer lehnen die Absicherung solcher Fahrzeuge schlicht ab. Ihnen fehlt das Fachwissen, die Infrastruktur oder die Rückversicherungskapazität, um im Ernstfall für Schäden im Millionenbereich aufzukommen.

2.3 Warum Standard-Versicherungen oft nicht ausreichen

Wer glaubt, dass eine Vollkaskoversicherung für einen Lamborghini Aventador auch für einen Lamborghini Centenario funktioniert, irrt sich gewaltig. Selbst wenn beide Fahrzeuge von derselben Marke stammen, ist der Centenario mit seiner Limitierung auf 40 Exemplare weltweit und einem Neupreis von rund 2 Millionen Euro eine völlig andere Kategorie – mit anderen Risiken.

Hier sind drei zentrale Gründe, warum Standardversicherungen versagen:

1. Wertfeststellung ist unpräzise

Normale Versicherer orientieren sich am Listenpreis oder am Zeitwert. Doch was, wenn das Fahrzeug im Sammlermarkt längst das Doppelte oder Dreifache wert ist? Eine Versicherung auf Basis des falschen Werts bedeutet im Ernstfall: Totalschaden – aber nur Teilerstattung. Nur Spezialversicherungen arbeiten mit Wiederbeschaffungswerten auf Gutachtenbasis und passen den Versicherungsschutz bei Wertsteigerung dynamisch an.

2. Versicherungsbedingungen schließen zentrale Risiken aus

Was viele Halter nicht wissen: In klassischen Policen sind Trackdays, Fahrten auf Rennstrecken oder sogar exklusive Events oft vollständig vom Versicherungsschutz ausgeschlossen. Auch Transportfahrten – sei es auf dem Anhänger, per Luftfracht oder Container – sind selten abgedeckt. Dabei gehört genau das zur Realität vieler Hypercar-Besitzer.

Hinzu kommt: Bei Vandalismus, Naturkatastrophen oder Diebstahl greifen viele Standardversicherungen nur in engen Grenzen. Hypercars stehen jedoch überdurchschnittlich häufig im Fokus von organisierten Diebstahlbanden oder werden gezielt beschädigt – ein besonders bekanntes Risiko in Regionen wie Südfrankreich, Norditalien oder London.

3. Fehlende Sachverständige und Reparaturpartner

Nach einem Schaden zählt jede Minute – und jedes Teil. Doch was, wenn der Sachverständige des Versicherers noch nie ein Fahrzeug dieser Klasse gesehen hat? Oder wenn eine nicht-autorisierte Werkstatt eine Reparatur vornimmt, die den Sammlerwert ruiniert? Standardversicherungen kennen solche Szenarien nicht. Spezialanbieter hingegen arbeiten mit akkreditierten Gutachtern, OEM-zertifizierten Werkstätten und sogar internationalen Logistikdiensten zusammen.

Kapitel 3: Versicherungsarten für Hypercars im Überblick

Wenn du ein Hypercar besitzt – sei es ein Bugatti Chiron Super Sport, ein Pagani Huayra oder ein Rimac Nevera – reicht es nicht, einfach eine „Vollkasko“ abzuschließen. Die Realität sieht deutlich komplexer aus. Hypercar-Versicherungen setzen sich aus verschiedenen Bausteinen zusammen, die individuell angepasst werden müssen. Im Folgenden geben wir dir einen Überblick über die gängigen Versicherungsarten, die für dein Fahrzeug relevant sein können – und wo die Unterschiede liegen.

3.1 Haftpflicht, Teilkasko und Vollkasko – die Basis

Auch bei Hypercars beginnt alles mit den bekannten drei Säulen der Kfz-Versicherung. Doch ihre Ausgestaltung unterscheidet sich stark vom Standardmodell:

Haftpflichtversicherung

Gesetzlich vorgeschrieben, deckt sie Schäden ab, die du mit deinem Fahrzeug Dritten zufügst. Für Hypercars ist sie meist nicht das Problem – wohl aber die Höhe der Deckungssumme. Viele Halter entscheiden sich für freiwillig erhöhte Deckungssummen, oft bis zu 100 Millionen Euro, um im Ernstfall nicht persönlich zu haften.Teilkasko

Umfasst üblicherweise Schäden durch Diebstahl, Glasbruch, Brand oder Naturereignisse. Bei Hypercars wird jedoch genau geprüft, wo und wie das Fahrzeug gelagert wird. Manche Versicherer schließen offene Carports oder Tiefgaragen ohne Videoüberwachung aus.Vollkasko

Deckt zusätzlich selbstverschuldete Schäden ab. In der Welt der Hypercars muss sie jedoch oft erweitert werden – z. B. um Schäden durch Fahrfehler auf abgesperrten Privatstrecken oder bei exklusiven Veranstaltungen. Achte hier besonders auf den Geltungsbereich und auf etwaige Selbstbeteiligungen in fünfstelliger Höhe.

Wichtig: Diese Basisversicherung ist bei Hypercars oft nur der Anfang. Die wahren Risiken liegen meist außerhalb des klassischen Fahrbetriebs.

3.2 All-Risk-Deckung (Allgefahrenversicherung)

Eine All-Risk-Deckung ist das, was man sich im Alltag unter „rundum sorglos“ vorstellt – allerdings mit einem Preis. Diese Versicherung greift grundsätzlich bei allen denkbaren Schadensursachen, es sei denn, sie sind explizit ausgeschlossen. Typische Vorteile:

Schutz gegen nahezu alle externen Einflüsse (inkl. Vandalismus, Transportschäden, Bedienfehler)

Gültigkeit auch im Ausland und auf privaten Strecken, sofern vereinbart

Erstattung zum Wiederbeschaffungswert anhand eines regelmäßigen Wertgutachtens

Besonders für Sammler und Investoren ist diese Police interessant, da sie nicht nur finanzielle Verluste absichert, sondern auch den Werterhalt durch präzise abgesicherte Reparaturen ermöglicht.

Aber Vorsicht: Nicht alles ist automatisch abgedeckt. Rennteilnahmen, grobe Fahrlässigkeit und absichtliche Beschädigungen sind oft auch hier ausgeschlossen – oder nur mit Zusatzklauseln abgedeckt.

3.3 Trackday- und Event-Versicherungen

Trackday-Fahrten wie hier auf der Rennstrecke sind für viele Hypercar-Fans unverzichtbar – doch ohne passende Zusatzpolice oft nicht versichert.

Ein Bugatti ist gebaut worden, um gefahren zu werden – doch nicht jeder gefahrene Meter ist automatisch versichert. Vor allem Trackdays, also nicht-öffentliche Fahrveranstaltungen auf abgesperrten Rennstrecken, sind bei normalen Policen ausdrücklich ausgeschlossen.

Spezielle Trackday-Versicherungen decken:

Schäden am eigenen Fahrzeug

Schäden an Dritten (wenn nicht durch Veranstalter-Haftpflicht abgesichert)

Transport und Zwischenlagerung während des Events

Die Versicherung gilt dabei nur für die jeweilige Veranstaltung oder einen vorher definierten Zeitraum. Sie ist oft teuer, aber bei Fahrzeugen mit Werten über 1 Million Euro nahezu Pflicht, wenn du nicht ausschließlich als Ausstellungsstück sammelst.

Tipp: Manche Versicherer bieten sogenannte „Trackday-Pakete“ für Vielfahrer oder Sammler mit mehreren Fahrzeugen – auch als Jahrespauschale.

3.4 Transport- und Logistikversicherung

Ein Hypercar steht selten dauerhaft in der heimischen Garage. Viele Fahrzeuge werden regelmäßig auf Achse, auf dem Anhänger, per Luftfracht oder im Container bewegt – zu Messen, Concours-Veranstaltungen, Auktionen oder Service-Zentren.

Standardversicherungen schließen Transportschäden oft aus, insbesondere bei internationalem Versand. Deshalb brauchst du eine gesonderte Transportversicherung, die u. a. schützt vor:

Schäden durch Verladung oder Bewegung

Verlust oder Diebstahl während der Logistik

Verzögerungen oder Beschädigungen durch Dritte (z. B. Speditionen, Zoll)

Für internationale Sammler ist diese Police unverzichtbar. Sie kann auch Bestandteil einer All-Risk-Versicherung sein, muss aber oft gesondert beantragt und mit Routenangaben versehen werden.

Kapitel 4: Kostenfaktoren – Warum Hypercar-Versicherungen so teuer sind

Der Versicherungsschutz für ein Hypercar kostet nicht selten mehrere zehntausend Euro pro Jahr. Doch woran liegt das genau? Warum ist die Prämie für einen Ferrari SF90 Stradale oder Koenigsegg Jesko um ein Vielfaches höher als bei einem Porsche 911 Turbo S – obwohl beide Fahrzeuge schnell, teuer und leistungsstark sind?

Die Antwort liegt in einer Kombination aus Fahrzeugwert, Risiko, Seltenheit und individuellen Anforderungen. Wer verstehen möchte, warum Hypercar-Versicherungen so kostenintensiv sind, muss die verschiedenen Einflussfaktoren kennen, die den Beitrag bestimmen – und welche Rolle der Halter dabei selbst spielt.

4.1 Fahrzeugwert & Exklusivität

Der wichtigste Faktor bei der Prämienberechnung ist der Versicherungswert des Fahrzeugs. Bei Hypercars reden wir schnell über Summen zwischen 1 und 5 Millionen Euro, teilweise sogar darüber hinaus – etwa beim Bugatti Divo, Aston Martin Valkyrie oder einem Pagani Imola.

Einige Fahrzeuge steigen mit der Zeit im Wert, etwa aufgrund limitierten Angebots, Sonderserien oder prominenter Vorbesitzer. Für den Versicherer bedeutet das: selbst im Totalschadenfall muss ein Fahrzeug eventuell nicht nur ersetzt, sondern auch weltweit aufwendig beschafft werden – oft zum Sammlerpreis, nicht zum Neupreis.

Zudem handelt es sich bei Hypercars fast immer um Unikate oder Fahrzeuge mit Individualausstattung, die nicht ohne Weiteres rekonstruierbar sind. Dieser exklusive Charakter erhöht die potenzielle Schadenssumme – und damit auch die zu kalkulierende Rücklage des Versicherers.

4.2 Ersatzteilversorgung & Reparaturkosten

Ein weiteres zentrales Thema sind die enormen Reparaturkosten. Ein Schaden an einem Karbon-Monocoque, eine beschädigte Aktiv-Aerodynamik oder ein Hybrid-Batteriemodul mit Motorsporttechnik kann sechsstellige Summen verschlingen – selbst bei vergleichsweise „kleinen“ Schäden.

Hinzu kommt: Ersatzteile sind oft nur in begrenzter Stückzahl verfügbar und müssen teilweise aus dem Ausland importiert werden – mit entsprechenden Lieferzeiten und Aufschlägen. In manchen Fällen existieren bestimmte Komponenten gar nicht mehr neu und müssen individuell angefertigt werden.

Beispiel: Ein neuer Stoßfänger für einen Pagani Huayra Roadster kann je nach Ausstattung bis zu 70.000 Euro kosten – ohne Lackierung und Einbau.

Zudem verlangen viele Versicherer, dass nur in vom Hersteller zertifizierten Werkstätten gearbeitet wird. Das ist zwar im Sinne der Werterhaltung, bedeutet aber auch: höhere Arbeitskosten, längere Standzeiten und komplexere Logistik. Die Folge: erhöhte Prämien zur Absicherung dieser Risiken.

4.3 Sicherheits- und Abstellbedingungen

Wo und wie das Hypercar gelagert wird, spielt eine entscheidende Rolle bei der Prämienhöhe. Normale Garagen oder Stellplätze ohne Sicherheitskonzept reichen hier nicht aus. Viele Versicherer verlangen:

Einzelstellplatz in gesicherter, alarmgesicherter Umgebung

Videoüberwachung mit 24/7 Zugriff

GPS-Ortungssystem mit Diebstahlbenachrichtigung

Bewegungsmelder, Brandschutz und Zugangskontrolle

Je besser die Sicherheitsvorkehrungen, desto günstiger kann die Prämie ausfallen – denn das Risiko eines Einbruchs oder Diebstahls wird minimiert. Fehlen jedoch entsprechende Schutzmaßnahmen, wird die Police entweder teurer oder gar nicht angeboten.

Insbesondere in hochkriminalisierten Gegenden – etwa London West End, Südfrankreich oder Norditalien – sind verschärfte Anforderungen Standard.

4.4 Persönliches Risikoprofil des Halters

Nicht nur das Fahrzeug zählt – auch der Fahrer wird bewertet. Versicherer kalkulieren individuell auf Basis von:

Alter und Fahrerfahrung

Führungszeugnissen bzw. Vorversicherungsverhalten

Fahrleistung pro Jahr

Teilnahme an Trackdays oder Rennveranstaltungen

Zweit- oder Drittfahrzeugregelungen

Ein 60-jähriger Sammler mit abgeschlossener Fahrpraxis, klimatisierter Halle und kaum gefahrenen Kilometern zahlt deutlich weniger als ein 25-jähriger Unternehmer, der mit dem Fahrzeug auch mal den Nürburgring besucht.

Trackdays, aggressive Fahrweise oder hoher Verschleiß (z. B. häufiger Reifen- und Bremsentausch) wirken sich negativ auf die Prämienhöhe aus – besonders, wenn keine ergänzenden Spezialversicherungen abgeschlossen wurden.

Auch die Frage, wer das Fahrzeug fährt, spielt eine Rolle. Viele Hypercar-Policen gelten ausschließlich für den Fahrzeughalter. Bei Fahrten durch Dritte – etwa Chauffeure, Geschäftspartner oder Familienmitglieder – entstehen häufig Zuschläge oder Ausschlüsse.

Kapitel 5: Unterschätzte Risiken – was viele Besitzer nicht bedenken

Selbst wenn man glaubt, sein Hypercar „perfekt“ versichert zu haben, lauern viele Risiken im Kleingedruckten oder in Alltagssituationen, die überraschend teuer enden können. Gerade in der Welt der Hypersportwagen ist es ein Trugschluss, zu glauben, eine Vollkasko- oder All-Risk-Versicherung schütze in jedem Fall umfassend. Tatsächlich gibt es zahlreiche unterschätzte Risiken, die im Ernstfall entweder nicht versichert sind – oder zu massiven Konflikten mit dem Versicherer führen können.

5.1 Nicht abgedeckte Risiken im Kleingedruckten

Viele Hypercar-Besitzer verlassen sich auf das Schlagwort „Allgefahrenversicherung“ (All-Risk-Coverage) und glauben, damit sei jedes Risiko automatisch abgesichert. Doch auch diese Premium-Policen enthalten Ausschlussklauseln, die genau gelesen werden müssen.

Typische Ausschlüsse:

Rennveranstaltungen und Zeitmessungen

Selbst legale Trackdays ohne Zeitwertung können ausgeschlossen sein – sofern nicht separat versichert.Grobe Fahrlässigkeit oder Vorsatz

Wer bei Glatteis mit Slick-Reifen fährt oder das ESP absichtlich deaktiviert, handelt unter Umständen grob fahrlässig – und verliert im Ernstfall den Versicherungsschutz.Unberechtigte Nutzung

Wird das Fahrzeug von einer Person gefahren, die laut Police nicht zugelassen ist (z. B. ein nicht eingetragener Familienangehöriger), kann das zum Leistungsausschluss führen.Wertsteigerung ohne Meldung

Wenn der Marktwert des Hypercars steigt (z. B. durch Nachfrage oder Sammlerwert), aber der Versicherungswert nicht angepasst wird, kann es zu einer Unterversicherung kommen – mit dramatischen Folgen bei Totalschäden.

Oft gilt: Was nicht schriftlich eingeschlossen ist, ist im Zweifel ausgeschlossen. Daher ist es entscheidend, jede Police individuell zu prüfen – und auch regelmäßige Updates einzuplanen, etwa bei Wertveränderungen oder Nutzungsänderungen.

5.2 Schäden durch Fehlbedienung oder Trackdays

Hypercars verfügen über extreme Leistungsdaten und technische Feinheiten – Launch-Control, Race-Modi, aktives Aero-Setup oder Hybrid-Rekuperation erfordern hohes fahrerisches Können. Schäden durch Fehlbedienung, z. B. beim Schalten im manuellen Modus oder beim unsachgemäßen Nutzen des Race-Modus auf nasser Fahrbahn, sind bei vielen Versicherungen nicht abgedeckt.

Ebenso heikel: Trackday-Fahrten ohne separate Absicherung. Selbst wenn der Fahrer glaubt, „nur zum Spaß“ zu fahren, werten viele Versicherer das als motorsportähnliches Event. Kommt es zu einem Schaden, kann die Leistung verweigert werden – auch bei minimalem Fremdschaden oder einfacher Fahrbahnberührung mit der Leitplanke.

Manche Policen schließen sogar Schäden an Reifen und Bremsen grundsätzlich aus, obwohl diese bei Hypercars durch die hohe Belastung oft mehrere Tausend Euro kosten.

5.3 Mitfahrer- und Beifahrerrisiken

Ein oft übersehener Aspekt ist die Absicherung von Mitfahrern. Viele Versicherungen bieten nur begrenzten oder gar keinen Schutz für Beifahrer – vor allem, wenn das Fahrzeug außerhalb des öffentlichen Straßenverkehrs genutzt wird (z. B. auf Events oder im Ausland).

Beispiel: Ein Freund darf in deinem Lamborghini Revuelto bei einem Fototermin mitfahren – doch beim Ausweichen auf losem Untergrund entsteht ein Schleuderschaden mit Personenschaden. Ohne klare Regelung zur Beifahrerabsicherung droht dir als Halter im schlimmsten Fall eine private Haftung – zusätzlich zur Selbstbeteiligung oder Prämienerhöhung.

Besonders heikel: Wird ein Fahrgast bei einer nicht genehmigten Nutzung (z. B. auf einem abgesperrten Privatgelände) verletzt, kann die Versicherung vollständig aussteigen – selbst bei klarer Schuld des Fahrers.

Kapitel 6: Spezialversicherer und internationale Policen

Wer ein Hypercar besitzt, braucht einen Versicherungspartner, der mehr kann als standardisierte Tarifrechner bedienen. Denn klassische Versicherungen stoßen bei Millionenwerten, Rennstreckennutzung und internationalem Einsatz schnell an ihre Grenzen. Die Lösung: Spezialisierte Anbieter, die sich auf Luxus-, Sammler- und Hochleistungsfahrzeuge konzentrieren – häufig mit maßgeschneiderten Policen, persönlicher Betreuung und weltweiter Abdeckung.

Doch welche Versicherer bieten solche Leistungen? Wie unterscheiden sich Angebote innerhalb Europas, in Großbritannien oder den USA? Und wann sind sogar Offshore-Policen sinnvoll? All das klären wir in diesem Kapitel.

6.1 Anbieter, die sich auf Luxusfahrzeuge spezialisiert haben

In Deutschland, der Schweiz und Österreich gibt es nur wenige Anbieter, die wirklich Erfahrung im Bereich Hypercar-Versicherung haben. Sie arbeiten oft nicht direkt, sondern über exklusive Maklernetzwerke, die mit Sachverständigen, Gutachtern und Werkstätten vernetzt sind.

✅ Beispielversicherer im deutschsprachigen Raum:

Hiscox Deutschland

Einer der bekanntesten Spezialversicherer im Luxussegment. Bietet individuell zugeschnittene Policen für Sammlerfahrzeuge, seltene Einzelstücke und Rennfahrzeuge. Trackday-Optionen, Wertsteigerungsabsicherung und weltweiter Transport sind in vielen Paketen wählbar.Zürich Classic Car Versicherung (über spezialisierte Makler)

Eigentlich auf Oldtimer und Liebhaberfahrzeuge spezialisiert, doch bei Einzelanfrage auch offen für moderne Hypercars – besonders im Sammlerkontext.Helvetia Exklusiv

Über ihre Premium-Linie bietet Helvetia eine Lösung für „besondere Risiken“, auch im Bereich Supersportwagen. Eine gute Option für Kunden in der Schweiz.OCC Assekuradeur (Oldie Car Cover)

Obwohl primär auf Oldtimer fokussiert, betreut OCC über Partnernetzwerke auch limitierte Sonderfahrzeuge mit Sammlerwert – auf Basis von Marktwertgutachten und Spezialpolicen.Südvers Gruppe / Hendricks GmbH

Große Maklerhäuser mit spezialisierten „Private Risk“-Abteilungen, die individuelle Hypercar-Versicherungen bei internationalen Partnern wie Lloyd’s of London oder HDI platzieren.

Diese Anbieter prüfen in der Regel jede Anfrage manuell, erstellen einzelne Policen auf Kundenprofilbasis und integrieren auch exotische Anforderungen – etwa die Nutzung auf abgesperrten Flugfeldern oder Events mit Medienbeteiligung.

6.2 Unterschiede zwischen EU-, UK- und US-Versicherern

Je nachdem, wo sich dein Hypercar befindet, registriert ist oder gefahren wird, gelten unterschiedliche Voraussetzungen und Versicherungskulturen. Wer international unterwegs ist, sollte die regionalen Besonderheiten kennen – vor allem im Schadensfall.

🇪🇺 EU-Versicherungen

Innerhalb der EU gelten harmonisierte Mindeststandards für die Kfz-Haftpflicht. Für Hypercars jedoch bieten nur spezialisierte Versicherer länderübergreifende Pakete. Achte hier auf:

Gültigkeit bei temporärem Auslandsaufenthalt

Mitversicherung von Veranstaltungen, Transporten und Events außerhalb des Zulassungslands

Übersetzte Policen bei Schadensfällen im EU-Ausland

Grenzüberschreitender Schutz ist möglich, erfordert aber eine klare Absprache mit dem Versicherer und oft Zusatzdokumente (z. B. internationale Deckungskarte).

🇬🇧 Großbritannien

Der UK-Markt ist Vorreiter für Spezialversicherungen, insbesondere durch den Lloyd’s-Markt. Dort werden viele Policen über sogenannte Coverholder abgewickelt – das sind autorisierte Makler oder Agenturen, die im Namen von Lloyd’s agieren.

Bekannte Anbieter aus UK:

Adrian Flux – Sehr erfahrener Spezialversicherer für Exoten, Trackday-Fahrzeuge und Sammlerfahrzeuge.

Footman James – Traditionsreicher Anbieter mit Fokus auf wertvolle Klassiker und Sonderanfertigungen.

Mann Broadbent – Versichert auch Fahrzeuge für Film, Ausstellung oder Medienproduktion – inkl. Sonderrisiken.

Vorteil britischer Policen: Hohe Flexibilität, Wertdeckung statt Zeitwert und oft niedrigere Prämien bei sicherer Lagerung.

🇺🇸 USA

In den USA sind Versicherer wie Hagerty, Chubb, American Collectors Insurance und Grundys Marktführer im Luxussegment. Wichtig: Die Tarife unterscheiden stark zwischen den Bundesstaaten und hängen u. a. von Lagerbedingungen, Jahresfahrleistung und US-Führerschein ab.

Besonderheit: Agreed Value Policies, bei denen der Wiederbeschaffungswert vertraglich fixiert wird – ideal für Wertsteigerungen und Investitionsschutz.

6.3 Offshore-Versicherungen für Sammler

Für Sammler, die mehrere Fahrzeuge in unterschiedlichen Ländern besitzen – oft mit Wohnsitz im steuerlich attraktiven Ausland oder mit Lagerhallen in Monaco, Dubai oder auf den Kanalinseln – können sogenannte Offshore-Policen sinnvoll sein.

Diese Policen laufen oft über Rückversicherer mit Sitz in:

Guernsey oder Jersey

Cayman Islands

Liechtenstein

Lloyd’s of London

Vorteile:

Internationale Abdeckung mit weltweitem Schutz

Mehrsprachige Policen (z. B. Deutsch / Englisch / Französisch)

Anpassbare Schadensdefinitionen, z. B. für Trackdays oder VIP-Veranstaltungen

Steueroptimierte Prämienmodelle bei komplexem Wohnsitz-/Fahrzeugmix

Beispiel: Ein Investor mit Wohnsitz in Dubai, der einen Rimac Nevera in einer Halle in Deutschland stehen hat, kann über einen in Liechtenstein ansässigen Makler eine globale Versicherungspolice mit Transport-, Event- und Standzeitdeckung abschließen – inklusive direkter Kommunikation mit Spezialwerkstätten weltweit.

Achtung: Offshore-Policen sind meist nicht für Alltagsnutzer gedacht, sondern für Sammler mit mehreren Fahrzeugen, hoher Expertise und klarer Trennung von Fahr- und Ausstellungsnutzung. Zudem sind die Einstiegskosten hoch – unter 10.000 € Jahresprämie kaum realistisch.

Kapitel 7: Tipps für die richtige Absicherung deines Hypercars

Ein Hypercar zu versichern ist kein standardisierter Prozess – und genau das birgt Fallstricke. Die Wahl des Versicherers, die Ausgestaltung der Police und dein eigenes Verhalten als Halter können darüber entscheiden, ob du im Ernstfall geschützt bist – oder im schlimmsten Fall Millionenverluste riskierst.

Mit den folgenden Tipps und Fragestellungen bist du auf der sicheren Seite.

7.1 Darauf solltest du bei der Auswahl achten

Bevor du einen Vertrag unterschreibst, stelle sicher, dass der Versicherer nachweisliche Erfahrung mit Hochleistungsfahrzeugen oder Sammlerstücken hat. Wer bisher nur Teslas und BMW M-Modelle versichert hat, ist für einen Koenigsegg oder einen Pagani überfordert.

Checkliste für die Auswahl:

Kenntnis im Hypercar-Segment: Gibt es bereits Kunden mit ähnlichen Fahrzeugen?

Individuelle Wertgutachten statt pauschaler Zeitwertabsicherung

Globale Abdeckung für Transport, Ausstellung und Fahrten im Ausland

Zusatzoptionen für Trackdays, Mediennutzung oder Concierge-Service

Kooperation mit Hersteller-zertifizierten Werkstätten und Gutachtern

Tipp: Gute Versicherer nehmen sich Zeit für eine Beratung. Skepsis ist geboten bei "Sofort-Abschlüssen" ohne Rückfragen zum Abstellort, Nutzung oder Wertentwicklung.

7.2 Fragen, die du deinem Versicherer stellen solltest

Gerade bei Hypercars ist es entscheidend, gezielt nachzuhaken – oft zeigt sich erst im Gespräch, ob der Anbieter wirklich vorbereitet ist. Hier sind essentielle Fragen:

Wie wird der Fahrzeugwert im Schadensfall ermittelt?

– Agreed Value oder nur Wiederbeschaffungswert?Sind Trackdays oder private Fahrveranstaltungen mitversichert?

– Wenn ja: Welche Bedingungen gelten?Was passiert bei Wertsteigerung oder Sonderumbauten?

– Wird die Police automatisch angepasst?Ist der Schutz international gültig (z. B. bei Events in Dubai, UK, Monaco)?

Gibt es Einschränkungen bei der Fahrerlaubnis?

– Nur Halter? Auch Familienmitglieder oder Chauffeure?Wie schnell erfolgt im Schadensfall die Regulierung – und über wen?

Diese Fragen helfen dir, „Marketingversprechen“ von realem Leistungsumfang zu unterscheiden.

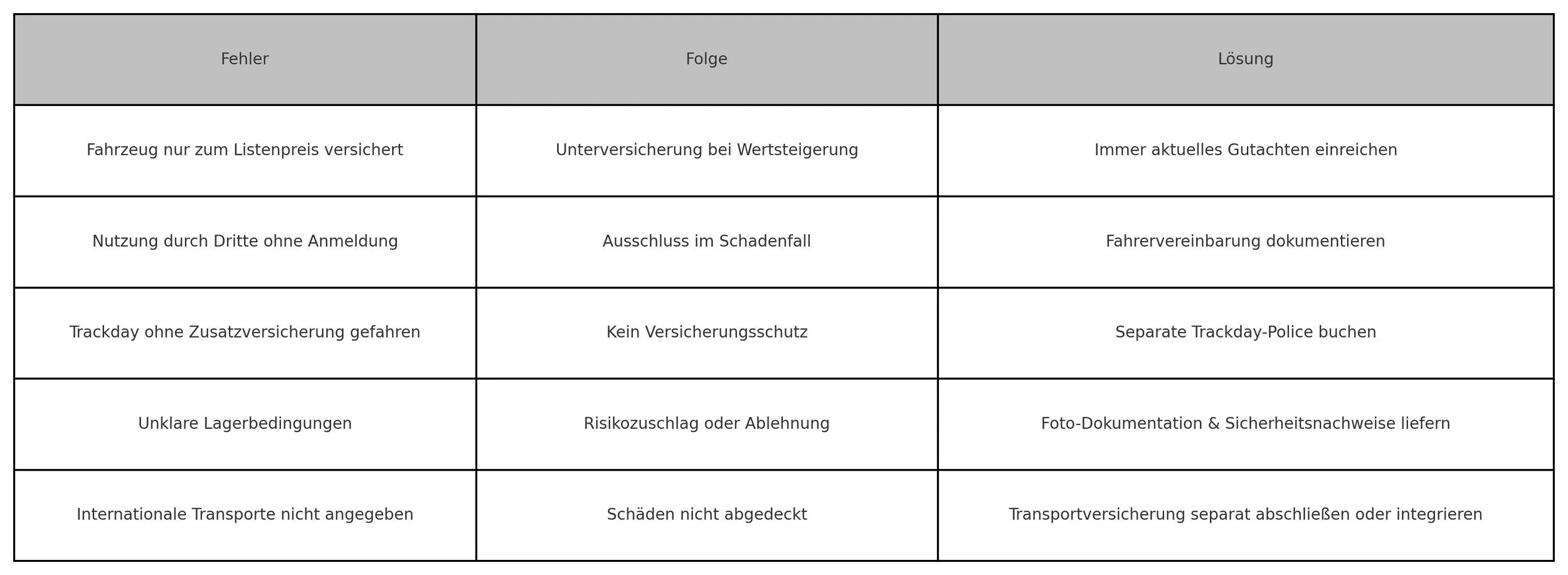

7.3 Typische Fehler bei der Absicherung – und wie du sie vermeidest

Auch erfahrene Halter tappen immer wieder in dieselben Fallen. Hier die häufigsten Fehler – und wie du sie vermeidest:

Kapitel 8: Versicherung und Investment – Wie Policen den Wert deines Hypercars beeinflussen können

Ein Hypercar ist nicht nur ein Fahrzeug – es ist in vielen Fällen ein Vermögenswert mit Wertsteigerungspotenzial. Modelle wie der Ferrari LaFerrari Aperta, der Bugatti Divo oder der McLaren Elva haben in kurzer Zeit beachtliche Marktwertzuwächse erzielt. Genau deshalb ist es entscheidend, dass die Versicherung nicht nur als Kostenfaktor betrachtet wird – sondern als strategisches Werkzeug zur Wertabsicherung und -steigerung.

8.1 Einfluss auf den Wiederverkaufswert

Beim Wiederverkauf eines Hypercars spielt der Zustand eine zentrale Rolle – und dieser ist eng mit dem Versicherungsverlauf verbunden. Käufer legen zunehmend Wert auf folgende Punkte:

Dokumentierte Schadenfreiheit (auch über Versicherungsnachweise)

Reparaturen ausschließlich bei OEM-zertifizierten Werkstätten

Lückenlose Nachweise über Wartung, Sicherheit und Standort

Individuelle All-Risk-Versicherungen als Vertrauensindikator

Ein potenzieller Käufer wird deutlich mehr Vertrauen in ein Fahrzeug setzen, dessen Absicherung professionell erfolgt ist. Viele Sammler und Investoren verlangen sogar explizit Versicherungszertifikate oder -historien, bevor sie hohe Summen investieren.

Zudem lassen sich durch bestimmte Policen – z. B. mit fester Wertvereinbarung (Agreed Value) – Dispute im Verkaufsfall vermeiden, etwa wenn es um die Bewertung bei Inzahlungnahme oder Auktion geht.

8.2 Versicherungsnachweise für Auktionen & Sammlerbörsen

Gerade bei renommierten Auktionshäusern wie RM Sotheby’s, Bonhams oder Artcurial sind Versicherungsnachweise mittlerweile Standard. Sie dienen dort nicht nur zur Objektbewertung, sondern auch als Vertrauenssignal für potenzielle Käufer.

Typischerweise angefragt werden:

Die aktuell gültige Police mit Versicherungswert

Nachweis über keine offenen oder unreparierten Schäden

Historie der abgesicherten Events oder Transporte

Bestätigung der Lager- und Sicherheitsstandards

Ein lückenhafter oder unvollständiger Versicherungsschutz kann nicht nur den Verkaufspreis drücken, sondern im schlimmsten Fall zur Ablehnung eines Loses bei hochwertigen Auktionen führen. Versicherungen fungieren somit auch als Reputationsinstrument im Luxusautomarkt.

8.3 Versicherung als Teil des Fahrzeugportfolios

Viele Hypercar-Besitzer besitzen nicht nur ein Fahrzeug – sie verwalten ein automobiles Anlageportfolio. In diesen Fällen wird Versicherung zur strategischen Komponente der Vermögensverwaltung.

Vorteile bei professioneller Einbindung:

Sammelpolicen für mehrere Fahrzeuge mit optimierten Prämien

Regelmäßige Wertgutachten zur Bewertung des Gesamtbestands

Absicherung seltener Einlagerungen, Transporte oder Rotationen zwischen internationalen Standorten

Vermeidung von Steuerkonflikten, wenn Versicherungen mit Wertzertifikaten kombiniert werden

Einige Versicherer bieten sogar Kooperationen mit Family Offices oder Vermögensverwaltern an, um Hypercars in bestehende Investmentstrategien zu integrieren. So lassen sich z. B. Liquiditätsreserven über beleihbare Policen absichern oder Fahrzeuge als alternative Anlageklasse mit dokumentierter Sicherheit erfassen.

Versicherungen erfüllen hier eine Doppelfunktion: Schutz im Schadensfall und Transparenz für Bewertung, Finanzplanung und Eigentümernachweise.

Kapitel 9: Praxisbeispiele & reale Schadensfälle

In der Theorie klingt Versicherungsschutz oft klar und nachvollziehbar – doch erst in der Praxis zeigt sich, wie entscheidend die richtige Police wirklich ist. Gerade bei Hypercars, deren Werte nicht selten siebenstellig sind, kann ein Schaden finanzielle und emotionale Konsequenzen nach sich ziehen, die weit über den reinen Reparaturbetrag hinausgehen.

In diesem Kapitel werfen wir einen Blick auf reale oder realitätsnahe Schadensszenarien, die zeigen, welche Fehler fatale Folgen hatten – oder wie gut abgesicherte Besitzer im Ernstfall gerettet wurden.

9.1 Der Fall eines McLaren P1 auf dem Track

Ein Unternehmer aus Frankfurt besaß einen McLaren P1 im Wert von ca. 1,4 Millionen Euro. Als passionierter Fahrer meldete er sich zu einem privaten Trackday auf dem Hockenheimring an. Was er übersah: Seine bestehende Vollkaskoversicherung schloss die Nutzung auf abgesperrten Rennstrecken explizit aus.

Beim Beschleunigen aus einer Kurve verlor er auf leicht feuchtem Asphalt die Kontrolle – das Fahrzeug krachte seitlich in die Leitplanke. Die Schäden: Front, Seitenschweller, Radaufhängung, aktive Aerodynamik – Reparaturkosten von über 270.000 Euro.

Doch der Schock folgte bei der Schadenmeldung: Die Versicherung verweigerte die Leistung, mit Verweis auf die Trackday-Klausel im Vertrag. Die Kosten musste der Halter selbst tragen – und zusätzlich den Wertverlust beim späteren Wiederverkauf akzeptieren.

Lektion:

Trackdays sind nicht automatisch versichert – selbst bei All-Risk-Policen. Wer auf abgesperrten Strecken fahren will, braucht eine separate, tagesgenaue Trackday-Versicherung.

9.2 Einbruch in eine Sammlerhalle in Monaco

Ein vermögender Sammler mit Wohnsitz in Monte Carlo ließ fünf seiner Fahrzeuge – darunter ein Bugatti Veyron Grand Sport Vitesse und ein Ferrari Enzo – in einer klimatisierten Halle mit Zugangskontrolle unterbringen. Trotz Sicherheitssystem wurde bei einer koordinierten Aktion eingebrochen – mehrere Fahrzeuge wurden beschädigt, zwei entwendet. Der Verlust lag bei über 6 Millionen Euro.

Die Versicherung griff – aber nur teilweise. Warum?

Die Halle war nicht rund um die Uhr videoüberwacht, wie in der Police gefordert

Ein Bewegungsmelder war seit Monaten außer Betrieb

Die GPS-Ortung der Fahrzeuge war bei dreien nicht aktiviert

Die Folge: Die Versicherung zahlte nur einen Teilbetrag – mit Hinweis auf Verletzung der Sicherheitsvorgaben. Der Halter musste den restlichen Verlust selbst tragen.

Lektion:

Versicherer leisten nur dann vollumfänglich, wenn alle vertraglich vereinbarten Sicherheitsvoraussetzungen erfüllt sind – im Zweifel zählt jeder Sensor. Bei Hypercars sind diese Anforderungen oft deutlich strenger als bei normalen Fahrzeugen.

9.3 Wie ein Versicherungsstreit einen Bugatti-Eigentümer fast ruinierte

Ein britischer Millionär hatte seinen Bugatti Chiron bei einem spezialisierten Londoner Versicherer mit einer sogenannten „Agreed Value Policy“ abgesichert – auf einen festgelegten Wert von 2,6 Millionen Pfund. Als ein nicht selbst verschuldeter Brand in der Tiefgarage ausbrach, wurde der Chiron stark beschädigt.

Doch der Versicherer verzögerte die Regulierung mit der Begründung, dass das Fahrzeug nicht regelmäßig bewegt wurde, wie in der Police vorgesehen. Der Halter hatte den Wagen über 12 Monate nicht gefahren – was laut Vertrag als „nicht vertragsgemäße Nutzung“ gewertet wurde.

Der Streit landete vor Gericht, und obwohl der Kläger am Ende recht bekam, dauerte der Prozess über zwei Jahre. Der Wiederverkaufswert des inzwischen reparierten Fahrzeugs war deutlich gefallen – und der Halter musste in der Zwischenzeit mehrere Millionen vorstrecken.

Lektion:

Auch bei scheinbar wasserdichten Policen wie „Agreed Value“ kann es bei unklaren Vertragsformulierungen oder fehlender Nutzung zu Leistungskonflikten kommen. Regelmäßige Nutzung oder explizite Stillstandsklauseln sollten schriftlich geklärt werden.

Kapitel 10: Fazit – Absicherung als Teil der Hypercar-DNA

Ein Hypercar zu besitzen bedeutet weit mehr, als nur ein Fahrzeug mit über 1.000 PS zu fahren. Es ist Ausdruck von Individualität, technischer Faszination, aber auch ein Investment mit hohem Risiko- und Wertpotenzial. Und genau deshalb ist die Versicherung nicht nur eine Pflichtaufgabe, sondern ein elementarer Teil des verantwortungsvollen Umgangs mit einem solchen Fahrzeug.

Viele Halter unterschätzen, wie komplex, individuell und lückenanfällig der Versicherungsschutz für ein Hypercar sein kann. Während eine Standard-Vollkasko für Alltagsfahrzeuge ausreichend sein mag, stoßen klassische Policen bei Pagani, Koenigsegg, Bugatti & Co. schnell an ihre Grenzen – oder werden im Ernstfall sogar zum Kostenfalle mit sechs- oder siebenstelligen Folgen.

Versicherung als strategisches Element – nicht nur als Schutzschild

Wer in ein Hypercar investiert, investiert nicht nur in Emotion und Leistung, sondern auch in einen potenziell wertstabilen oder sogar wertsteigernden Vermögenswert. Eine professionelle, individuell zugeschnittene Versicherung ist damit kein reiner Risikoschutz, sondern:

Teil einer strategischen Portfolioverwaltung

Vertrauensgarantie für Käufer, Auktionatoren und Gutachter

Schutz für Events, Transporte und internationale Nutzung

Basis für den Werterhalt bei Unfällen oder Reparaturen

Je nach Nutzung – sei es als Alltagsfahrer, Trackday-Enthusiast oder reiner Sammler – müssen die Versicherungsbausteine maßgeschneidert zusammengesetzt werden. Standardlösungen helfen hier nicht weiter.

Die größten Gefahren lauern oft im Detail

Wie die Praxisbeispiele zeigen, sind es oft kleine Unachtsamkeiten, die zu existenzbedrohenden Problemen führen: ein fehlender GPS-Tracker, ein nicht aktivierter Bewegungsmelder, eine Klausel zur Rennstreckennutzung, die überlesen wurde.

Gleichzeitig zeigt sich: Wer professionell vorgeht, mit Spezialmaklern arbeitet, Verträge jährlich überprüft und die Nutzung transparent dokumentiert, kann selbst komplexe Risiken wirksam absichern – und im Ernstfall schnell und unkompliziert Ersatz erhalten.

Verantwortung beginnt vor dem Startknopf

Ein Hypercar ist mehr als ein Fortbewegungsmittel – es ist eine Verpflichtung. Wer ein Fahrzeug dieser Klasse steuert, trägt Verantwortung: für sich, für andere und für den Werterhalt eines automobilen Kunstwerks. Diese Verantwortung zeigt sich nicht nur auf der Straße, sondern auch auf dem Papier – im Versicherungsvertrag, im Sicherheitskonzept und in der Transparenz gegenüber dem Versicherer.

Die Devise lautet: Lieber zu viel fragen, als zu wenig versichern. Und: Versicherungsschutz ist kein Nebenschauplatz, sondern ein integraler Teil des Hypercar-Erlebnisses.